As a compliance officer, you play a crucial role in safeguarding your firm against regulatory risks. Building a robust compliance culture is essential not only for regulatory adherence but also for maintaining the trust of your clients and stakeholders. To help you with this vital mission, here are valuable pointers on establishing a strong compliance culture within your financial advisory firm.

Establish Clear Policies and Procedures

A strong compliance culture starts with well-defined policies and procedures that align with regulatory requirements. Ensure that these guidelines are accessible and clearly communicated to all employees. Remember to review and update your policies regularly to include any changes in the regulatory environment.

Promote Proactive Email Monitoring

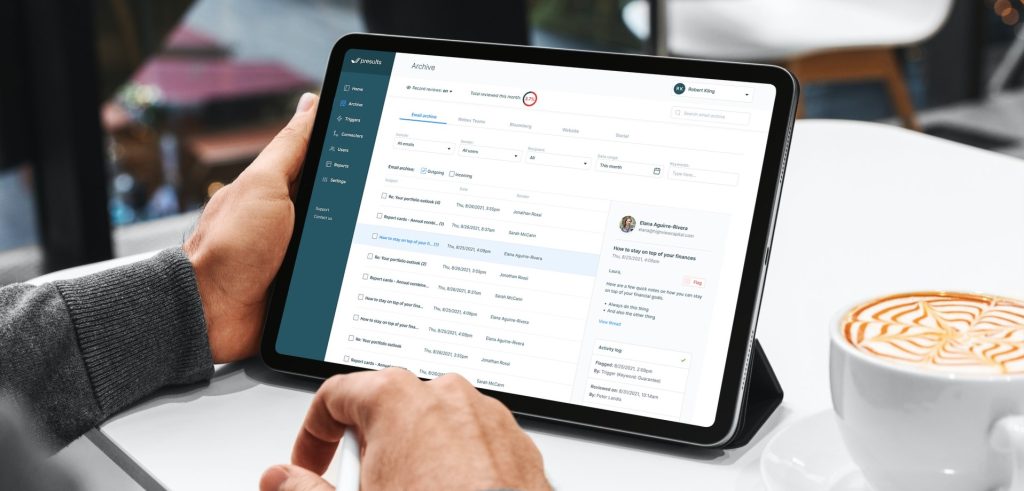

Email communication is a significant area of risk for financial advisors. Implementing proactive email monitoring software, such as Presults, can help identify and mitigate potential compliance breaches. Presults automatically scans and flags emails that contain non-compliant keywords before they get sent to the client.

Regular Reviews of Client Communication

Conduct regular reviews of client communications to ensure adherence to regulatory requirements. With vast amounts of communications to review and consistently changing regulations, it’s recommended to invest in technology to aid in internal reviews. For example, Presults can reduce the manual time spent on email reviews by 90%.

Foster a Culture of Accountability

Compliance is the responsibility of everyone. Achieving this involves keeping employees informed about the latest regulatory updates and best practices, and providing them with both human and technological support. Presults educate advisors about compliance by informing them when words or key terms they want to use are non-compliant.

Leverage Modern Technology for Compliance Management

When it comes to building a strong compliance culture at your advisory firm, it’s important to invest in modern technology solutions that can streamline compliance management processes. Just as you keep your website up-to-date, you should also ensure that your compliance software is modern and equipped with the latest technological advancements, such as automation and AI.

It’s essential to evaluate your compliance tools to make sure they are up-to-date with the ever-changing digital communication platforms that clients expect.

Ready to Enhance Your Compliance Culture?

Building a robust compliance culture is an ongoing journey that requires commitment and the right resources. At Presults, we offer comprehensive solutions designed to support your compliance efforts. Schedule a demo with our experts today to learn how we can help you achieve a robust compliance culture.

Selecting the right archiving solution for your financial advisory practice is crucial. It’s not just about ticking boxes; it’s about finding a solution that enhances compliance, efficiency, and overall effectiveness. Here are five key considerations to keep in mind:

1. Comprehensive Archiving Capabilities

Ensure that your chosen archiving solution can handle all facets of your communication. While email archiving is fundamental, modern advisory practices often extend communication to websites and social media. Thus, a tool that solely archives emails may fall short of your compliance requirements.

Selecting an archiving solution that neglects to capture your clients’ preferred digital communication channels can prove detrimental. It not only hampers your ability to utilize those platforms compliantly but also jeopardizes the overall client experience.

2. Proactive Compliance Measures

Look for solutions that offer proactive compliance features rather than relying solely on reactive measures. Solutions like Presults, with its built-in compliance lexicon and real-time email monitoring, can prevent non-compliant communication from ever being sent, reducing the need for retrospective reviews.

Time is a precious resource for financial advisors, and it’s much better spent on client-facing work than on compliance tasks. Seek tools equipped with automation, such as automated archiving or AI-powered solutions that can efficiently flag compliance concerns in real time. Automation is a cost-efficient way to free up valuable time for advisors to focus on providing a better client experience.

4. Price Transparency and Flexibility

Speaking of cost-efficiency, price is a crucial factor to consider when seeking an archiving solution, but it’s not just about the monthly fee. Consider additional hidden charges like storage, import/export fees, and setup costs. Importantly, scrutinize export fees, as they can become significant cost, especially with outdated legacy archiving solutions. Opt for platforms such as Presults that offer flexibility, such as month-to-month contracts, and free data exports to avoid being locked into unfavorable arrangements.

5. Accessible Customer Support

In the world of technology, reliable customer support can be a game-changer. Prioritize providers that offer personalized onboarding and accessible customer support. Ask about onboarding assistance, training opportunities, and the availability of direct communication with support staff. Avoid platforms known for poor support, as they can exacerbate any issues you encounter.

Specific questions to ask a provider include:

• What does your onboarding support look like? • What training do you offer to new customers? • If I have questions, will I have the ability to speak directly to a person? • What methods of communication do you offer for customer support? Phone? Chat? Email?

The Takeaway for Advisors Selecting an Archiving Solution

Investing time and effort into selecting the right archiving solution can pay dividends in the long run. By considering factors like comprehensive capabilities, proactive compliance measures, automation, pricing transparency, and customer support, financial advisors can find a solution that not only meets their compliance needs but also enhances operational efficiency. Choose wisely to streamline your advisory practice and mitigate future challenges.

Effective archiving is a cornerstone of compliance for financial advisory firms. Yet, many stumble into common archiving pitfalls that hinder compliance, reduce efficiency, and jeopardize client trust. In this article, we’ll delve into the five most prevalent archiving mistakes financial advisory firms make and how to avoid them.

Mistake #1: Thinking it’s one person’s responsibility

Archiving is often seen as a task assigned to one individual or department. However, it’s a collective responsibility that requires coordination across the organization to ensure that all team members are taking a responsible and proactive approach to compliance.

To ensure that archiving and compliance are seen as the responsibility of everyone, education is key. While educating employees on archiving best practices may seem like another task you just don’t have time for, you can leverage AI to proactively monitor team members’ communication with clients to proactively notify and educate them on non-compliant communication.

Manual archiving is inefficient and prohibits growth.

Mistake #2: Archiving everything manually in your financial advisory firm

Manual archiving of everything is inefficient, it leaves your advisory firm prone to errors and increases the risk of oversight and non-compliance. Compliance is not an area where you can afford to make mistakes. Financial advisory firms must embrace automated compliance solutions to minimize compliance risks. In addition, automation streamlines the archiving process and empowers teams to focus on high-value tasks to drive business growth.

Mistake #3: Not being proactive with archiving

Financial advisory firms often fall into the trap of being reactive instead of proactive by waiting until after non-compliant communication surfaces before addressing the issue. This approach not only increases stress levels but also exposes the firm to compliance headaches and potential regulatory penalties.

Proactive archiving solutions, on the other hand, implement real-time email monitoring systems that actively scan communications for non-compliant keywords or terms. By staying ahead of the curve, firms can identify and rectify potential compliance issues before they escalate into more significant problems, ensuring smoother operations and peace of mind.

Mistake #4: Not having data easily accessible for audits

When auditors come knocking, quick and easy access to archived data is paramount. Fumbling through disorganized files or outdated systems can delay audits and raise red flags. Financial advisory firms are often required to provide comprehensive documentation and evidence of their compliance efforts during audits, such as archived communications and other relevant data. Without efficient archiving systems in place, firms may struggle to locate and retrieve the necessary information, wasting valuable time and resources and increasing audit times.

To avoid these pitfalls, financial advisory firms must prioritize the accessibility and organization of their archived data. This involves implementing robust archiving solutions that offer centralized storage, advanced search capabilities, and user-friendly interfaces. By consolidating archived data in a secure and easily accessible repository, firms can streamline the audit process and maintain regulatory compliance.

Mistake #5: Using outdated archiving technology in your financial advisory firm

Legacy archiving solutions may struggle to keep pace with evolving regulatory requirements and technological advancements. Investing in modern archiving technology is not just about compliance; it’s about enhancing security, scalability, and efficiency. By leveraging cutting-edge archiving solutions, financial advisory firms can future-proof their compliance efforts and adapt to changing regulatory landscapes with ease.

Modern archiving solutions provide scalability to accommodate the growing volume of digital communications and data generated by financial advisory firms. As the industry evolves and client demands shift, scalable archiving solutions allow firms to adapt seamlessly without compromising performance or compliance standards. Ultimately, investing in a modern archiving solution goes beyond mere compliance—it’s a strategic decision to fortify the firm’s infrastructure, optimize operational efficiency, and enhance client trust.

Final Thoughts

In the fast-paced world of financial advisory services, avoiding common archiving mistakes is critical to ensure compliance, streamline the audit process, improve your firm’s efficiency, and maintain client trust. By avoiding these five common archiving mistakes and embracing modern solutions, financial advisory firms can navigate regulatory complexities with confidence, safeguarding their reputation and fostering long-term success.

Over the past few years, social media has played an important role in the wealth management industry’s marketing efforts, presenting opportunities for advisors to attract new clients and keep up with existing ones.

By being active and posting regularly on the various social media channels, advisors are able to directly communicate with their clients, and present themselves as competent stewards of their hard-earned money. But as with any area of advertising, social media comes with compliance concerns, including archiving.

In this article we’ll explore how advisors take advantage of the opportunities social media provides, while also fulfilling their compliance requirements.

Being active on social media can have a major impact on client count and total AUM

Why Should I Be Active on Social Media?

Social media is no longer only for young people. According to Pew Research Center, 70% of US adults are active on social media. And while younger generations were earlier adopters, older generations are catching up. Forty-five percent of Americans 65 years and older are active on at least one social media platform and 73% of those 50-64. In short, advisors should be active on social media because their clients and prospective clients are active on social media.

One reason advisors may be hesitant to devote resources to social media is because they want a clearer ROI. Social media often lacks the immediate and direct response in sales of some other forms of advertising, but that doesn’t mean it’s not valuable. A well-crafted social media strategy is an important part of any advisors marketing plan. Social media provides opportunities to build brand awareness, connect more directly with both clients and prospective clients, and build credibility.

But as with any form of marketing, not every strategy is a good strategy. The key to successful implementation of a strategy is intentionality.

Which platforms are a good fit? You don’t need (or want) to be on every possible platform.

What separates you from the competition? Share content that highlights your unique knowledge and experience.

What is the brand image you wish to portray? How will your social media highlight this?

What different kinds of content will you share? Include some variety to keep your posts more engaging.

The other reason advisors may be holding back from actively engaging in social media is due to concerns regarding compliance. While compliance is something that must be addressed, it’s no reason to miss out on all the benefits social media can provide. The first step to remaining compliant is knowing exactly what’s expected.

What Are the SEC and FINRA Requirements for Social Media?

Here we will cover some of the key requirements for social media, but compliance is complex, and advisors should always review any issues or concerns with their compliance personnel.

The biggest thing to keep in mind when creating content for social media is that it’s a form of advertising and as such, the same rules that apply to any other form of advertising also apply to social media. If you couldn’t put it on your website or in your marketing materials, you can’t put it on social media.

Though the rules are the same, the application of those rules isn’t always clear cut. Social media is still new, and regulators have struggled to apply the rules in such a way that aligns with this new form of marketing.

For example, in December of 2020, the SEC released its much anticipated new Investment Advisor Marketing Rule. The rule went into effect on May 4, 2021, though compliance action will not begin until November 4th, 2021.

Prior to the new marketing rule, advisors could not include testimonials. The rule addressed the changing nature of how people use and interact with companies online and updated these rules so that advisors can now include testimonials from clients, including both reviews and referrals. To avoid having these be misleading, compensation for the testimonial or any conflicts must be disclosed. This brings the SEC guidelines more in line with those of FINRA, which also allows firms to share testimonials, as long as the firm discloses if the individual providing the testimonial was compensated.

The other area that applies to social media, just like any other form of advertising, is recordkeeping. Both the SEC and FINRA have rules that require advisors to keep records of their advertising. In practice, this means advisors must find ways to archive their social media.

What Happens if I Don’t Archive My Social Media Posts?

Advisors who don’t archive their social media posts are in violation of their recordkeeping requirements. In other words, they’re not in compliance.

Both the good and the bad news, depending on how you choose to look at it, is that there’s not one specific consequence for advisors not in compliance. If the SEC were to conduct an exam and audit your firm, the consequences could vary. You could receive a deficiency, which does not come with any fines or penalties, or the auditor in charge of your exam could choose to make an example of you and fine you heavily. While the latter is less likely, it’s possible, and taking on the extra risk when there are such simple solutions makes little sense.

Regardless of the consequences, staying in compliance is always your best bet. Finance is a heavily regulated industry, and while this may add additional burdens on the vast majority of advisors who work in their clients’ best interests, the industry does have bad actors too. Sadly, regulations are necessary in order to keep the handful of bad actors from harming their clients.

What Social Media Channels Can I Archive?

Just as advisors must archive their website and emails, they must also archive their social media. But “social media” covers a wide range of platforms and content. What exactly should advisors archive?

The short answer is pretty much everything. Remember, everything you put on social media is an advertisement, and advertisements require that you keep records of them.

The good news is that you can archive content from any social media platform. The other thing advisors will want to keep in mind is that it’s not just posts on social media that require archiving, any comments are also part of their advertising and therefore require archiving.

Now that we’ve covered what advisors need to do, now we’ll consider how they can go about doing it. Many advisors have heard of some of the larger names in archiving, but plenty of other options also exist, including Presults.

Social Media Archiving is Included with Email Archiving

As we’ve seen, while email archiving is important, so is social media archiving. Many other archiving platforms have a basic package that includes only email archiving with additional fees for archiving your website or any social media sites. That’s not the case with Presults. Presults includes both website and social media archiving in its basic package.

Monitor Emails Before They’re Sent

Most archiving solutions allow you to flag for keywords in outgoing emails, but they do so only after the email has been sent. While this is better than nothing, it means you’re addressing issues instead of keeping them from happening. Presults is different.

Presults allows advisors to monitor emails with potentially non-complaint emails before they’re sent. The advisor simply needs to include a list of keywords to flag, and every outgoing email is auto swept and flagged. Not only does Presults help address issues before they arise, but it also eases the burden of email review.

More Bang for Your Buck

Everyone wants a fair price, but for smaller advisors the costs of remaining compliant may prove especially challenging. Additionally, many larger archivers force advisors into long-term contracts, which may not be a good fit for the advisor.

Presults understands the value of flexibility and believes in retaining customers by providing a valuable product and excellent customer service, not long contracts that are difficult to get out of. Presults offers a month-to-month subscription that includes email, social media, and website archiving starting at under $100 per month.

Built Specifically for Financial Advisors

Many industries have recordkeeping requirements, but advisors have unique needs. That’s why Presults was specifically built with the specific requirements of advisors in mind. Furthermore, as the regulatory landscape continues to evolve, Presults will continue to offer services that help advisors meet their needs.

With the needs of advisors in mind, in addition to its comprehensive base package, Presults also offers add-on features that help meet the needs of advisors, including email encryption, client personal information protection (such as SSNs and DOBs), and tone detection, which can provide a warning when conversations are becoming too heated.

In Conclusion

Social media provides new ways for advisors to engage with existing clients and build brand recognition with prospective clients. Compliance concerns shouldn’t keep you from taking advantage of this potential opportunity. Cost effective, user friendly options such as Presults can help you engage in social media while remaining compliant.

Clients must trust their financial advisor for the advisor/client relationship to work. If you’re an advisor, that means handling your clients’ money responsibly, but in this day and age, it also means protecting your clients’ data. The problem is that keeping clients’ data secure isn’t always easy, and best practices are always evolving. Here’s how you can stay up to date on the best ways to protect and securely share data with clients.

What Data Must Advisors Protect?

Before we talk about protecting client data, we first need to take a step back and discuss what sort of data requires protection. Personally Identifiable Information (PII) is information, either sensitive or non-sensitive, that either on its own or in combination with other information, can be used to identify an individual. Social security numbers, driver’s licenses, and financial information are all examples of sensitive PII. Other types of PII are non-sensitive, but when used in conjunction with other data could also identify an individual. Date of birth, zip code, and place of birth are all examples of non-sensitive PII. Ideally, advisors will protect all PII, but sensitive PII is especially important to protect and should only ever be shared securely.

Sharing Files Securely

The nature of the financial advisory business requires the sharing of much PII and other sensitive information. Therefore, one of the hardest parts of protecting client data is figuring out how to send and receive data to and from clients. To make clients more amenable to any additional steps imposed by your cybersecurity policy, instead of framing cybersecurity as a regulatory requirement or a hassle, frame it as another aspect of your excellent customer service – something you want to go above and beyond on because you value securing the data of your clients.

End-to-End Encryption

One of the most common ways to protect data is through encryption. To send and receive sensitive information, you need encryption on both ends, which is called end-to-end encryption. This method of sharing data works so well because only the sender and receiver can decrypt the shared information and therefore are the only ones who can view the contents. While end-to-end encryption is a great option, it’s largest drawback has typically been that implementation is required on both ends, meaning that to share information with a client, that client must sign up for the encryption service. While not terribly difficult, this process may prove time consuming for the client.

Presults offers an innovative approach to this obstacle by utilizing a combination of auto-expiring pages and one-time verification codes that don’t require client registration.

Cloud Storage

Another option for sharing information with clients securely is through cloud storage. The point of storing documents on the cloud is to keep those documents from being stored on your computer’s hard drive (which is typically more vulnerable). The benefits of cloud storage extend beyond more securely sharing and protecting data. When documents are stored on the cloud you can access them from any device with an internet connection, which allows for easier collaboration on documents and eliminates the risk of losing documents if a specific computer is damaged, lost, or stolen.

Client Portal

The final option for securely sharing sensitive data with clients is a client portal. A client portal is a centralized, secure area where clients can login to view communications, reports, invoices, contracts, etc. A client portal is a great option from a customer service perspective since the burden on clients is minimal. The only downside is that not all portals allow for two-way communication, though some do. If you value two-way communication, you’ll therefore want to find an option that includes this offering.

Train Employees on Client Privacy

According to a report by the Financial Planning Association’s Research and Practice Institute, 44% of advisors say they don’t understand the risks and issues of cybersecurity. This is especially concerning considering that while 48% of data breaches were due to malicious or criminal attacks, a full 27% of data breaches were due to human error. Proper training is therefore necessary both to decrease the risk of human error, and to make it harder for hackers to take advantage of weaknesses in your cybersecurity. While education obviously can’t eliminate human error, it can help decrease the chances of it.

The proper training for you and your employees will depend on the various roles of those in the firm. Mandatory training should be required for everyone, which goes over the firm’s procedures for protecting client data. The reason why these procedures are necessary should also be included in the training. How do your procedures help limit the chances of a data breach? What would a data breach mean for the company? What would a data breach mean for the information and assets of clients?

Create a Plan for a Data Breach

No matter what precautions you implement or how well you educate your team, a data breach is still possible, which is why every firm should create a data breach emergency plan. Every plan will be unique, but should include the following: • Data recovery procedures • How you will notify clients of the breach • Procedures for compensating clients impacted by the breach.

For a more personalized plan, work with your IT team or IT consultant. The more quickly you can react to a data breach, the better, both for your firm and for your clients. Becoming aware of the breach quickly, notifying clients immediately, and communicating exactly how you will handle the data breach can help maintain clients’ trust in you and your firm.

Another option that may be worth considering is cybersecurity insurance. Depending on the specific plan, this type of insurance could help you cover costs related to data recovery and compensating clients.

The Takeaway

Advisors have a duty to their clients, and that includes doing their best to protect client data. Presults takes protecting client data seriously, which is why its unique software flags emails containing PII and keeps them from being sent out. Unlike most other email archiving systems on the market, which only notify you after PII has been sent out, Presults gives you the ability to proactively protect the valuable data of your clients.